What are the New California Laws?

California recently passed two climate disclosure and financial reporting laws, SB 253 and SB 261, which will require firms of certain sizes that conduct business in the state to assess and report on climate-related considerations, including greenhouse gas (GHG) emissions figures and material financial risks related to climate. ESG and climate-related disclosures have come into focus for companies and policy makers as stakeholders increasingly recognize climate-related impacts on businesses. Regulations like SB 253 and SB 261 are intended to allow for more consistent, comparable, and reliable climate risk information from corporates operating under the remit of these laws.

SB253: Climate Corporate Data Accountability Act

• Requires firms generating over $1 billion in gross annual revenue to report annually on their scope 1, 2, and 3 GHG emissions figures

• Represents the first legal requirement in the US at either the state or federal level for companies to report on scope 3 emissions, which often represent the majority of a company’s carbon footprint as a result of activities upstream or downstream the value chain

• Many non-California firms may also indirectly be impacted due to scope 3 reporting requirements

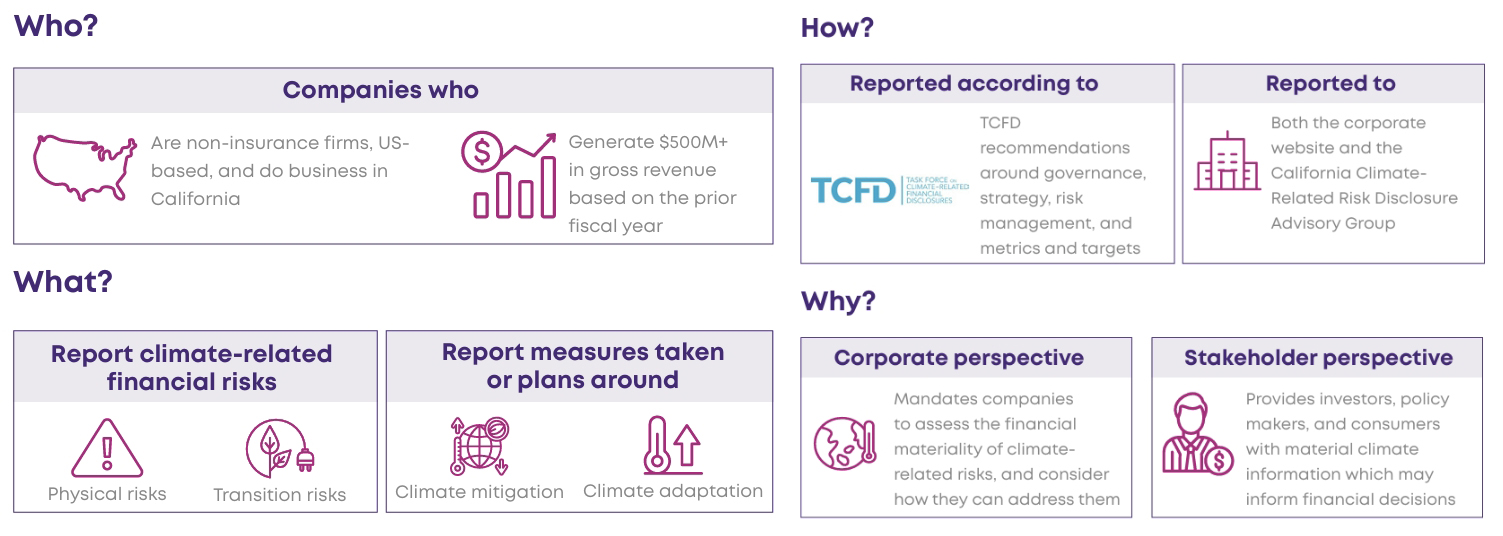

SB261: Climate-Related Financial Risk Act

• Requires firms generating over $500 million in gross annual revenue to report biennially on financially material climate-related risks, as well as measures adopted or planned to mitigate or adapt to such risks

• Will improve transparency around climate-related considerations for investors, policy makers, and other stakeholders who undertake financial decisionsrelated to California firms

SB 253– Climate Corporate Data Accountability Act

SB 253 requires firms generating over $1 billion in gross annual revenue to report annually to the California Air Resource Board (CARB) on their GHG emissions, or face up to $500,000 in penalties from CARB.

SB 261– Climate-Related Financial Risk Act

SB 261 requires firms generating over $500 million in gross annual revenue to report biennially on climate- related financial risks and measures to mitigate or adapt to them, or face up to $50,000 in penalties from CARB.

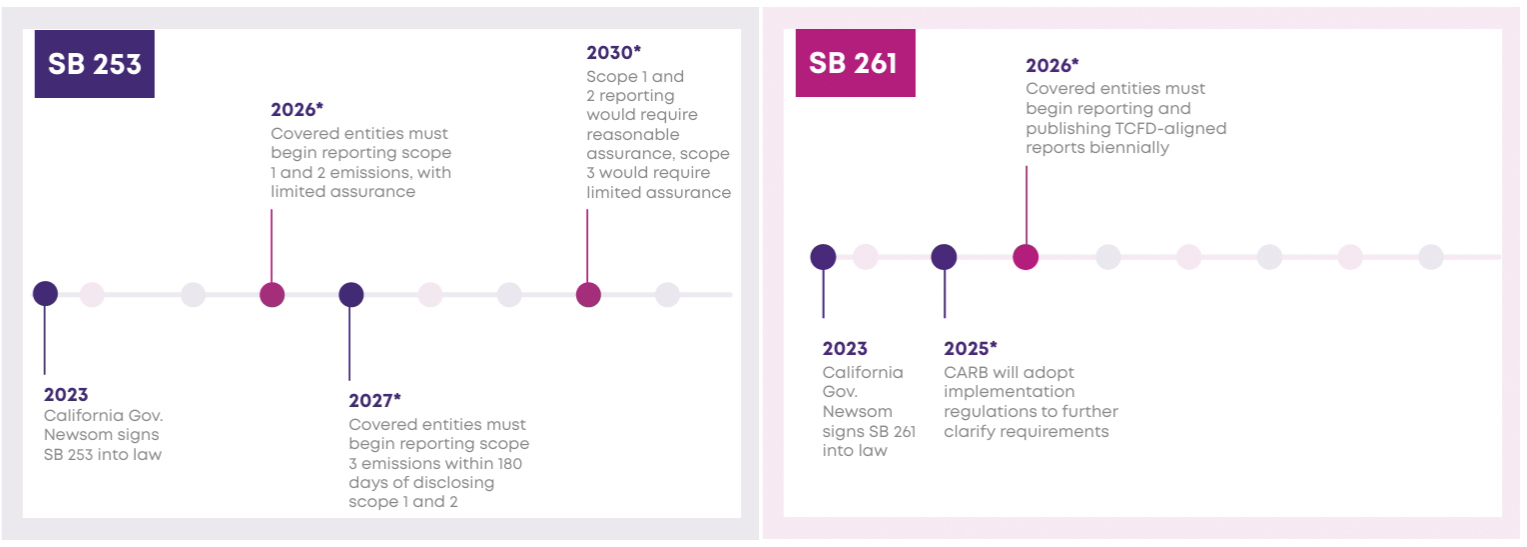

Phase-in Timelines

Uniqus Interpretations and Perspectives

SB 253 and SB 261 host complex reporting requirements, and therefore much clarification remains to be developed by policy makers to effectively finalize these regulations. Uniqus has provided its initial interpretations and perspectives on the California climate disclosure laws, and is monitoring regulatory changes closely. Uniqus will provide updates as interpretations of these laws continue to develop.

The laws are silent with respect to how the revenue thresholds are to be calculated. Uniqus interprets that revenue for the purpose of SB 253 and SB 261 would be the revenue reported by an entity in the US at a consolidated level. For example, a corporation which has five subsidiaries in the US, the consolidated revenue of which exceeds $1 billion, has to apply SB 253, assuming that it does business in the state of California. Further, in our view, for non-US parent companies, revenue thresholds should be considered based on consolidated revenues of US-based entities (which could include a standalone reporting entity in the US or a US-based holding company).

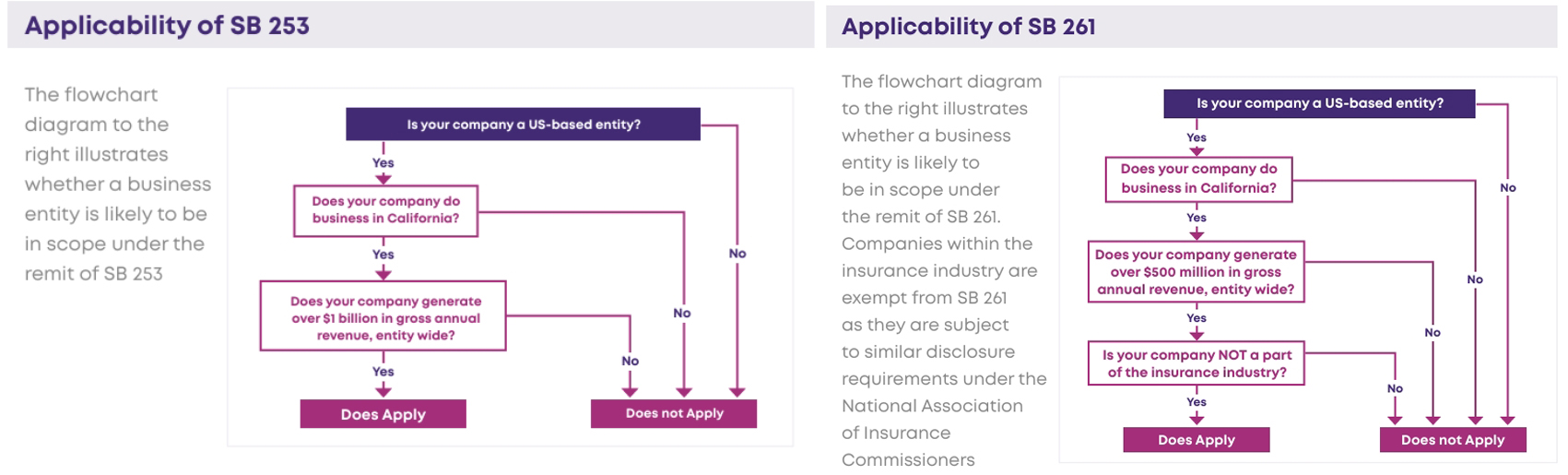

What does ‘doing business in California’ mean?

‘Doing business in California’ is not explicitly defined within the current context of SB 253 or SB 261. Uniqus interprets this definition based on the state’s business entity laws, under the California Corporations Code, and tax laws, under the California Revenue and Taxation Code. The below flowchart diagram illustrates whether a business is ‘doing business in California’ under its business entity and tax laws. Should the definition be clarified and expanded to companies that have any economic nexus to California whatsoever, Uniqus will update its interpretation.

Interoperability with other Climate Disclosure Regimes

While these laws represent one of the first large scale regulatory efforts within the US for companies to report climate-related disclosures, there are additional proposals and regimes that exist across other jurisdictions which require similar disclosures. For example, the EU’s Corporate Sustainability Reporting Directive (CSRD) mandates a sustainability reporting framework — which includes climate risks, impacts and goals — upon all large EU businesses, listed SMEs, and foreign companies with substantial EU activity. The US SEC also proposed climate-related rules which would require public US companies to disclose climate risks, track greenhouse gas emissions, and provide details around climate-related goals, if any are established.

Differences with the SEC’s Proposed Climate Rules

California’s two climate laws have similar requirements and intended effects as the SEC’s proposed climate disclosure rules, but aspects of implementation differ — namely regarding the extent and applicability of requirements. Uniqus is closely monitoring the SEC’s proposal, as well as interactions with California’s laws which may impact finalization.

Cost of Compliance and Preparation

Similar to regulations like the CSRD, California’s climate regulations incorporate a principal of proportionality. Gathering, verifying, and disclosing climate-related information can be quite costly, given the associated complexities and time requirements across different business stakeholders, operations, and value chains. SB 253 and 261 apply to companies generating over $1 billion and $500 million in gross annual revenues, respectively, meaning that the laws will only apply to larger public and private companies doing business in the state. California’s regulations therefore preliminarily consider the cost of compliance and have established applicability thresholds that should help ensure that undue burdens are not placed upon smaller companies, which may not have the capabilities and budgets to adequately comply. However, additional work is being conducted by California policy makers to assess the cost of compliance with both regulations, which will be taken into account as the laws’ phase-in dates are being finalized.

Way Forward

Uniqus Consultech offers a variety of capabilities to help businesses prepare for California’s climate disclosure requirements and similar regulatory developments, including comprehensive carbon accounting, ESG reporting, and ESG techenablement services. As interpretations of California climate-related disclosure laws continue to unfold, companies should be proactive in developing and refining their disclosure capabilities with respect to key elements of these laws, namely quantification of Scope 1, 2 and 3 greenhouse gas emissions and processes for addressing TCFD recommendations.

Key Takeaways

All firms generating at least $500M in gross revenue and doing business in California must prepare to meet climate-related reporting requirements, including material risks and GHG emissions, if not doing so already. Businesses outside of the remit of SB 253 may also be subject to client requests around reporting scope 1 and 2 emissions, as customers themselves could flow down their own scope 3 emissions disclosure requirements. Companies should start the process of interacting with their internal and external stakeholders familiarising them with the likely implications of reporting data under these laws. Further, the impact of disclosures needs to be understood in the context of ESG ratings. Companies need to be cognizant of the risks associated with the ratings process. Implications on collating information will require talent to be nurtured within the organizations.. Companies need to build capacity of their teams such that there is an understanding and appreciation of the requirements of disclosures under the law.